MTAR Technologies Limited was incorporated in the year 1999 in Hyderabad. The company serve customers in the clean energy, nuclear and space and defence sectors where it manufactures critical and differentiated engineered products with a healthy mix of developmental and volume-based production. Thus, the offerings are customized to meet the specific requirements of its customers. Since inception, company have strived to grow continuously, contributing to the Indian civilian nuclear power programme, Indian space programme, Indian defence, and aerospace sector, as well as to the global clean energy sector and the global defence and aerospace sector. Over the years, it has also developed import substitutes such as ball screws and water lubricated bearings that are specialized and used in the sectors the company cater to.

The company’s engineering capabilities has evolved over decades, and enabled them to consistently offer quality precision manufactured components and assemblies, within stipulated timelines and at reasonable cost in most cases, thus allowing them to forge a robust relationship with their customers. Order Book as on Dec 31, 2020 in the clean energy sector, the nuclear sector and the space and defence sectors stands at Rs 80.19 Cr, Rs 93.19 Cr, and Rs 160.61Cr, respectively.

Other details about the company:

Top 3 customers: Bloom Energy, NPCIL and ISRO

7 Manufacturing Facilities: Hyderabad and Telangana

Aggregate Order Book as on Dec 31, 2020: Rs 336.20 Cr

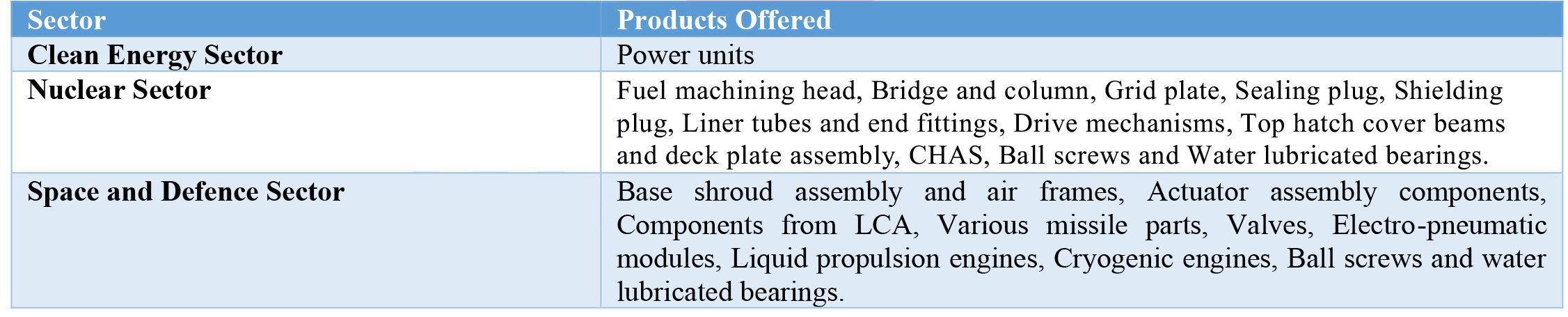

Product Portfolio:

STRENGTHS OF THE COMPANY

• Precision engineering expertise with complex product manufacturing capability – MTAR uses high precision quality inspection equipment such as 3D Co-ordinate Measuring Machines (“CMM”), laser measuring, optical alignment instruments, non-contact measuring, and other such non-destructive testing equipment to ensure ideal quality, as requested by the customers. Capability in measuring and maintaining quality and measurement records at each level of the process is a key enabler for the company. Its operations are supplemented by R&D over the years, which are undertaken primarily for manufacturing processes.

• Diversified product portfolio – The company offers wide range of products to its customers, which help to maintain long-standing relationships with its customers. Major product portfolio includes 3 kinds of products in the clean energy sector, 14 kinds of products in the nuclear sector and 6 kinds of products in the space and defence sectors.

• Strong and diversified supplier base for sourcing of raw materials – The company has, over the years, developed a robust supply chain for the sourcing of a wide variety of specialized raw materials used in the manufacture of mission critical precision products. Given that raw material expenses constitute a significant portion of overall cost, ~42% of the revenue, company benefit majorly from a strong, spread out and diversified supplier base, which enables them to negotiate favourable terms and even avail better discounts.

STRATEGIES ADOPTED

• Continue to expand product portfolio with higher margins – The company entered new business segments such as establishment of sheet metal facility and enhancement of existing specialized fabrication capabilities that will be used to cater existing and new customers. As the demand for clean energy is going to rise significantly, it has commenced manufacturing electrolyzers to produce methane-free hydrogen which can be used in multiple sectors to generate power.

• Expand international presence including through increase in exports – The company intends to reach out to global OEMs who either currently have defence deals with India or have their business operations in India. It is also planning to enter defence offset partnership with certain global OEMs and have incorporated its subsidiary, Magnatar Aero Systems Private Limited in this regard.

• Increase market share both through organic and inorganic growth – The company has consistently grown its manufacturing and production infrastructure through internal accruals. It aims to acquire capabilities such as electrical and electronics, which are complementary to its operations, and thus recently entered partnership with an entity in the electronics field. In addition, any potential acquisition in the future will revolve around enhancing its engineering competencies, increasing its market share in the industry and enhance profitability.

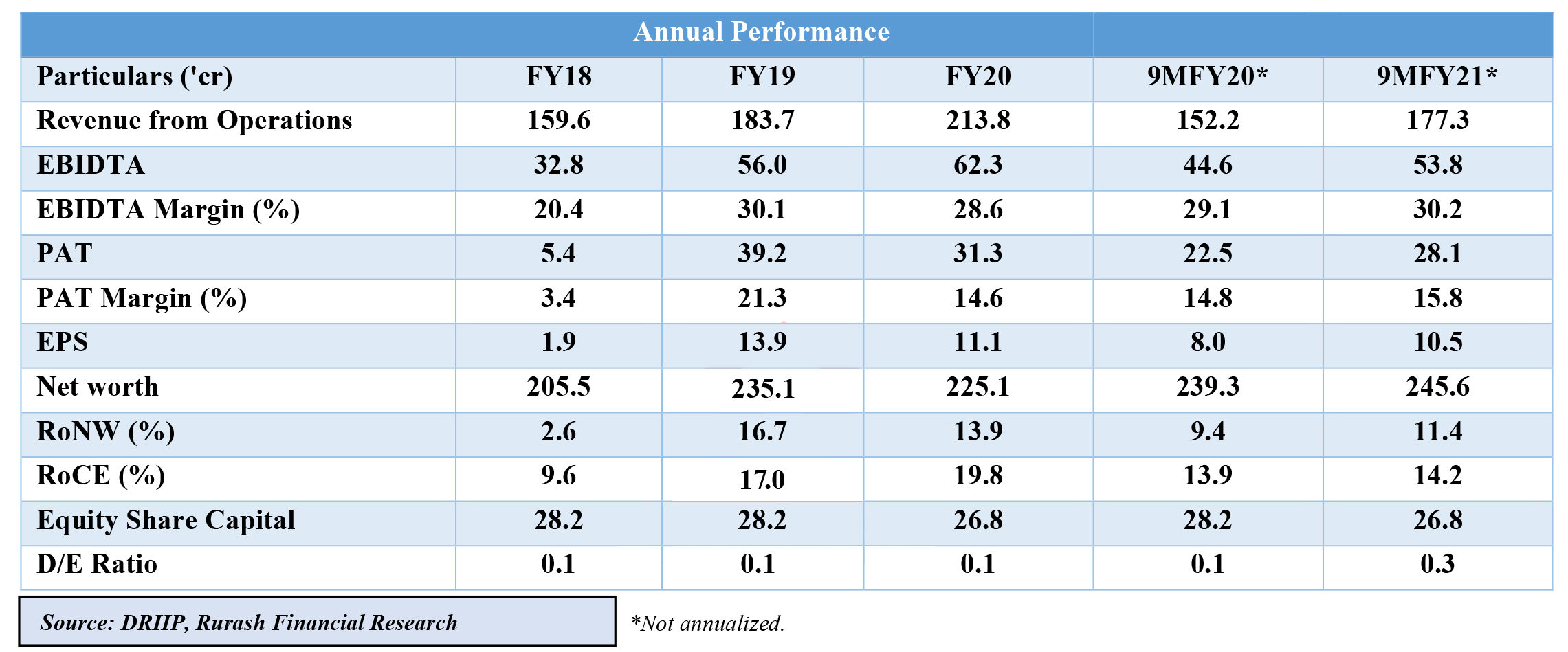

FINANCIAL SNAPSHOT

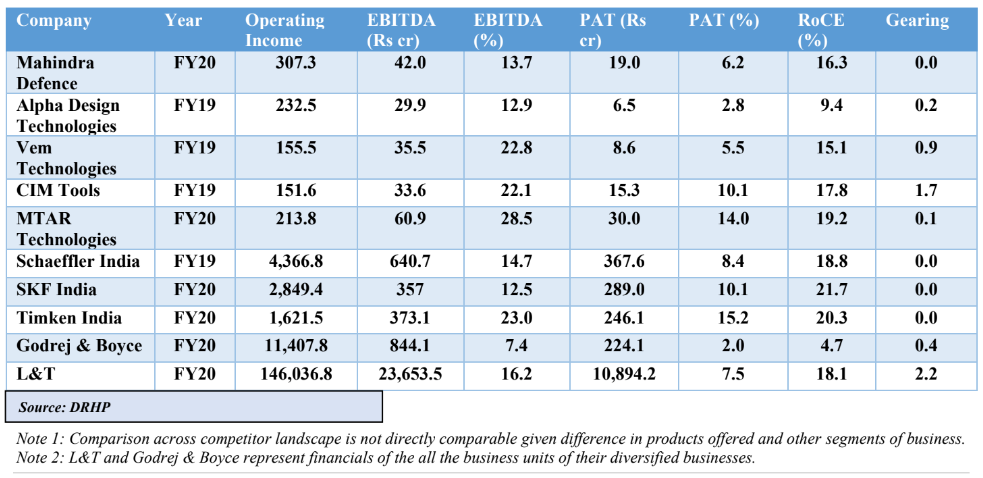

PEER COMPARISON

OUR ANALYSIS AND RECOMMENDATION

The domestic precision engineering industry’s turnover is estimated at Rs 4,415 Bn for FY2019, clocking CAGR of 7.1% over FY16-20. This growth will be further enhanced in the next 5-10 years due to Make in India initiative and sector-specific initiatives to boost manufacturing. Thus, MTAR operating in clean energy, nuclear or defence possess a strong favourable outlook in India. This is well supplemented by the Government’s boost for domestic sourcing and self-reliant especially in self-defence space. The company, having the high-tech engineering capabilities over the years, is rightly placed to capture the opportunities lying ahead in the industry in comparison to its peers. Company can supply technologically advanced products to not only Indian customers but foreign customers as well. Currently, revenue from exports is ~54%, with a major customer being US Based Company, Bloom Energy. Company is into development stage of manufacturing roller screws and once successfully done, will be the first manufacturer in India to supply its products to customers in defence, aerospace and clean energy space. Recently, GOI has sanctioned manufacture of 10 fleet reactors, which is the next big opportunity for the company. Thus, the demand for its products is huge and company being the leader in complex precision engineering will have an upper hand to take full advantage of the opportunity lying ahead.

Company’s current order book is ~1.6x of FY20 revenue, with ~48% of its orders coming from space and defence sector. Also, company plans to pay most of its debts from the funds raised through IPO, which will make company almost debt-free. In addition, the financial growth in the last 3 years has been robust with revenue and profit growing by 16% and 140% CAGR over FY18-20. Thus, the healthy order book, growth opportunities, financial performance, stable client base, limited direct competition, places company in the beneficial position in the industry. However, 80% of its revenue comes from the top 3 customers, highlighting high concentration risk. In addition, the company’s major customer are public-sector companies like NPCIL, DRDO, ISRO, etc, where the payments received have always been delayed, thus company has high receivables in its book Management has indicated to expand its business segment and look to increase export, where we believe this will eventually result in expansion of its customer base.

From the valuation perspective, the company is commanding a PE of 52x of its FY20 EPS and 41x of its FY21E EPS. Government’s top priority for the industry, no direct peer in the industry (although company may face competition threat from Germany and US) and clear visibility of its revenue due to large order book, the price asked for by the company, is justified to some extent.

DISCLAIMER

This article is prepared by CA Shraddha Jain, Senior Research Analyst – Unlisted & Private Equity, on February 16, 2021. The views expressed herein are based on the facts and assumptions indicated in the document.

All investment / financial opinions and/or views expressed herein are the personal views of the author. All the information contained herein is to be construed as indicative data which has to be corelated with actual market and economic conditions.

It is very important for investors to do their own analysis before making any investment. The investor should take independent financial advice or independently research and verify, any information herein. The information contained in the report is not intended as, and shall not be understood or construed as, financial advice.

Unintended and misprints may occur despite best efforts to ensure that all information is accurate and up to date. Please remember at all times that –

- Investment in unlisted securities is subject to market risks.

- Unlisted securities do not offer an easy exit route, such as selling on stock exchange, as in the case of listed securities.

- Any future gains or losses indicated herein are projections, based on our understanding of the market and macro economic situation as well as our understanding of the enterprise issuing the unlisted securities, as on the date of this communication. Future course of events may change the projections. We do not assume responsibility to update this report based on such changes.

- We do not guarantee any profits, losses or rate of return.

Connect with our team of experts to know all about RailTel Corporation of India Limited IPO now. Call now or drop a mail to invest@rurashfin.com.